12 / 43

12 / 43

AL MAZAYA HOLDING COMPANY K.S.C. (CLOSED) AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2008

(All amounts are in Kuwaiti Dinars)

Amended lAS 27 Consolidated and Separate Financial Statements (2008)

Amended lAS 27, which will be effective for annual periods beginning on or after July 1, 2009 with

retrospective application, requires accounting for changes in ownership interests by the Group in a

subsidiary, while maintaining control, to be recognized as an equity transaction. When the Group losses

control of a subsidiary, any interest retained in the former subsidiary will be measured at fair value with

the gain or loss recognized in the consolidated statement of income.

IFRIC Interpretation 11 "IFRS 2 - Group and Treasury Share Transactions"

The application of IFRIC Interpretation 11, which will be effective for annual periods beginningon or after

March 1, 2007, provides guidance as to whether certain share options given to employees should be

accounted as an equity-settled or cash-settled transaction.

Amendments to IFRS 2 Share-based Payment- Vesting Conditions and Cancellations

Amended IFRS 2, which will be effective for annual periods beginning on or after January 1, 2009 with

retrospective application, clarifies the definition of vesting conditions, introduces the concept of non-

vesting conditions, requires non-vesting conditions to be reflected in grant-date fair value and provides

the accounting treatment for non-vesting conditions and cancellations.

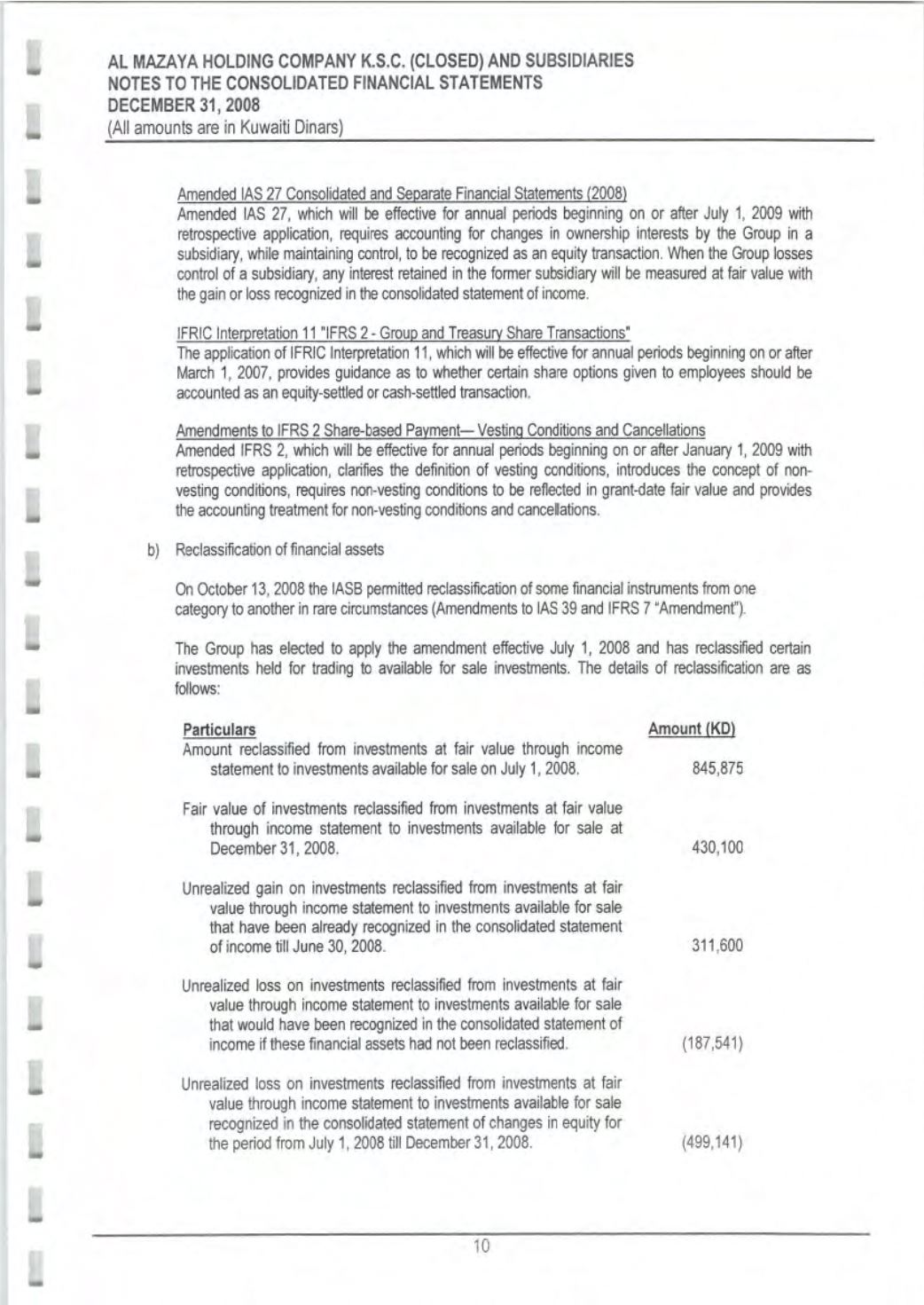

b) Reclassification of financial assets

On October 13, 2008 the IASB permitted reclassification of some financial instruments from one

category to another in rare circumstances (Amendments to lAS 39 and IFRS 7 "Amendment").

The Group has elected to apply the amendment effective July 1, 2008 and has reclassified certain

investments held for trading to available for sale investments. The details of reclassification are as

follows:

Particulars

Amount (KD)

Amount reclassified from investments at fair value through income

statement to investments available for sale on July 1

f

2008.

845,875

Fair value of investments reclassified from investments at fair value

through income statement to investments available for sale at

December 31, 2008.

430,100

Unrealized gain on investments reclassified from investments at fair

value through income statement to investments available for sale

that have been already recognized in the consolidated statement

of income till June 30, 2008.

311,600

Unrealized loss on investments reclassified from investments at fair

value through income statement to investments available for sale

that would have been recognized in the consolidated statement of

income if these financial assets had not been reclassified.

(187,541)

Unrealized loss on investments reclassified from investments at fair

value through income statement to investments available for sale

recognized in the consolidated statement of changes in equity for

the period from July 1,2008 till December 31,2008.

(499,141)

10